Payment processing can sometimes seem confusing or intimidating to merchants, especially for new entrepreneurs. To help you understand better and make informed decisions, we’ve compiled a list of the top 15 common payment processing terms every merchant should know. Understanding these terms will be incredibly helpful for managing your payment processes efficiently and ensuring smooth, secure transactions.

-

Merchant Account

Definition: A merchant account is a specialized bank account that enables businesses to accept and process electronic payment card transactions, including credit and debit cards. It is typically set up through a merchant acquiring bank.

A merchant account acts as the intermediary between your business and the customer’s bank account. It ensures that payments are transferred securely and efficiently. Think of it as the cornerstone of your payment processing operations.

-

Payment Gateway

Definition: A payment gateway is a service that securely transmits credit card information from a website to the credit card network for processing. Then it returns the transaction details and responses back to the website.

It serves as the virtual equivalent of a point-of-sale terminal. This ensures that your customers’ data is encrypted and secure during online transactions. Choosing a reliable payment gateway is critical for the safety and efficiency of your e-commerce operations.

-

Acquirer (Acquiring Bank)

Definition: An acquirer, or acquiring bank, is a bank or financial institution that processes credit and debit card payments on behalf of the merchant. The acquirer is responsible for settling funds with the merchant.

Essentially, your acquiring bank helps ensure all card transactions are processed flawlessly. This can have a direct impact your cash flow and overall financial health.

-

Issuer (Issuing Bank)

Definition: The issuer, or issuing bank, is the bank or financial institution that provides the customer with a payment card (credit or debit). The issuer is responsible for paying the acquirer for approved transactions.

The issuing bank acts as the customer’s financial protector. It ensures that funds are available for the transaction and managing any potential disputes or fraud claims. Understanding the issuer’s role can provide insight into the entire payment ecosystem.

-

Chargeback

Definition: A chargeback is a reversal of a credit card transaction initiated by the cardholder’s bank, often due to disputes over non-authorized transactions, dissatisfaction with products/services, or fraud.

Chargebacks can be detrimental to your business, leading to potential revenue losses and damaging your merchant account standing. Employing strategies to minimize chargebacks is key to maintaining a healthy merchant account.

-

Interchange Fee

Definition: The interchange fee is a fee paid between banks for the acceptance of card-based transactions. Typically, the merchant’s bank (acquirer) pays the issuing bank this fee to cover handling costs, fraud risk, and credit risk.

Interchange fees form the backbone of fee structures in the payment processing industry. Understanding these fees can help you budget more effectively.

-

Payment Processor

Definition: A payment processor is a company that handles the transaction process between merchants, financial institutions, and customers, ensuring that payments are securely and efficiently transferred.

The payment processor works behind the scenes, making sure that transactions are authorized, funds are settled, and any potential issues are quickly resolved. Choosing the right payment processor can impact the reliability of your operations.

-

Authorization

Definition: Authorization is the process of verifying whether a customer’s payment method has sufficient funds and is approved for the transaction. This is the initial step in processing a payment.

Securing authorization is akin to a checkpoint in the transaction journey. Without this approval, the transaction cannot proceed, making it a critical step in ensuring smooth and secure payment processing.

-

Settlement

Definition: Settlement is the process of transferring funds from the customer’s issuing bank to the merchant’s acquiring bank, finalizing the payment after authorization.

Settlement marks the completion of the transaction cycle, converting pending authorizations into actual payments in your account. Efficient settlement processes are vital for maintaining healthy cash flow.

-

Point of Sale (POS)

Definition: The point of sale, or POS, is the location or system where a transaction takes place between a merchant and a customer, typically involving a physical or virtual terminal that processes payments.

Your POS system bridges the gap between the customer’s intent to purchase and the actual payment. A robust POS system can enhance customer experiences and streamline operations.

-

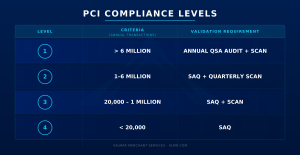

PCI Compliance

Definition: PCI compliance refers to adhering to the Payment Card Industry Data Security Standard (PCI DSS), a set of security standards designed to ensure that all entities that process, store, or transmit credit card information maintain a secure environment.

PCI compliance is non-negotiable for any business handling credit card transactions. It safeguards against data breaches, ensures customer trust, and helps avoid hefty penalties.

-

Rolling Reserve

Definition: A rolling reserve is a security measure by which a percentage of a merchant’s revenue is held back by the payment processor for a certain period to cover potential chargebacks, refunds, or fraud.

While the concept of a rolling reserve might seem daunting, it’s a measure designed to protect both the merchant and the payment processor. Understanding how it works can help you manage your cash flow and financial planning more effectively.

13. Payment Facilitator (PayFac)

Definition: A Payment Facilitator is a company that allows small businesses to accept card payments without having to set up their own direct merchant account with a bank. Instead, the PayFac manages the relationship with the processor and “onboards” businesses under its master account. This makes setup faster, though it usually comes with higher fees, more risk, and less customization than a traditional merchant account.

14. Interchange-Plus Pricing

Definition: Interchange-Plus Pricing is a transparent fee model where the processor passes along the actual interchange rate (the non-negotiable cost set by card networks) plus a fixed markup. For example: interchange fee + 0.25% + $0.10 per transaction. Business owners like this model because they can see exactly what goes to the card networks versus what goes to the processor.

15. Fixed Rate / Flat Rate Pricing

Definition: Fixed Rate (or Flat Rate) Pricing means every transaction is charged the same percentage and per-transaction fee, no matter the card type. For instance, 2.9% + $0.30 per sale. This model is simple and predictable, but it can hide the true underlying costs, making it more expensive for businesses with higher volumes or many debit card transactions.

Understanding these 15 common payment processing terms can significantly contribute to smoother transactions and more informed financial planning for your business. At Valmar, we are committed to providing transparent pricing, exceptional customer service, and reliable payment processing solutions, even for high-risk industries. Understanding these key terms will empower you to take full advantage of our services and foster a more secure and efficient payment environment for your business. Reach out to us for any queries or assistance in optimizing your payment processing system.

Our dedicated team cares about our clients as individuals and business owners. It’s challenging to operate and grow a business, so we provide resources and support for our merchant clients. With enough other concerns, you shouldn’t have to worry about your payment processing. (Especially if you’re in a high-risk industry.) At Valmar, we give our merchants a level of comfort, clarity, and peace of mind unrivaled in payment processing with next level customer service. If you want a payment processor that cares about you, contact us—we’re here to help!