The functional mushroom industry is booming, but when it comes to payment processing, most brands quickly hit a wall.

Whether you’re selling lion’s mane, reishi, amanita muscaria, or mushroom-infused products, your business is often categorized as “high-risk” by traditional payment processors. That means higher scrutiny, frequent account shutdowns, and limited access to reliable payment solutions.

In this guide, we’ll break down the best payment processors for functional mushroom brands, what to look for, and how to avoid costly mistakes.

Why Functional Mushroom Brands Are Considered High-Risk

Even though functional mushrooms are legal, payment processors still flag them due to:

- Regulatory gray areas (especially with wellness claims)

- Overlap with CBD, nootropics, or alternative health products

- Higher-than-average chargeback risk

- Evolving compliance standards

This is the same reason CBD and supplement companies struggle with payments – many banks and processors simply don’t want the risk exposure.

As a result, mainstream platforms like Stripe, PayPal, and Square often:

- Freeze funds without warning

- Shut down accounts abruptly

- Hold reserves

What to Look for in a Mushroom Payment Processor

Not all payment processors are built for high-risk wellness brands. The best providers offer:

1. High-Risk Merchant Account Support

You need a dedicated merchant account, not a payment aggregator. This ensures:

- Stable processing

- Individual underwriting

- Reduced risk of sudden shutdowns

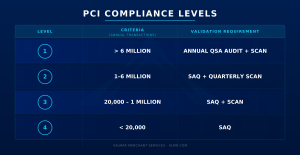

2. Compliance & Risk Monitoring

Functional mushroom brands must follow strict guidelines around:

- Product labeling

- Marketing claims

- Ingredient transparency

A good processor helps you stay compliant, not just approved.

3. Chargeback Prevention Tools

High-risk industries face stricter thresholds (often under 1%).

Look for:

- Fraud filters

- Chargeback alerts

- Clear billing descriptors

4. Transparent Pricing

Expect:

- Clear disclosure of all fees and pricing structures

- Possible rolling reserves

But avoid hidden fees or unclear contracts.

Best Payment Processors for Functional Mushroom Brands

Valmar Merchant Services (Best Overall)

If you’re selling functional mushrooms, especially alongside CBD or smoke shop products, Valmar is purpose-built for your industry.

Learn more here: https://stage.vlmr.com/mushroom-payment-processing/

Valmar specializes in high-risk merchant accounts designed specifically for:

- Functional mushroom brands

- CBD and alternative wellness products

- Smoke shops and online retailers

Unlike traditional processors, Valmar offers:

- Stable, long-term payment processing

- Reduced risk of account shutdowns

- Transparent pricing with no surprises

- Dedicated support for high-risk businesses

Best for: Brands that want reliability and scalability without constant payment disruptions.

Other Providers to Consider

PaymentCloud

PaymentCloud is a high-risk processor that some newer supplement and wellness brands explore during the early stages of growth.

Potential limitations can include reserve requirements, changing bank placements, and less specialization in mushroom-specific businesses.

PayKings

PayKings supports several high-risk industries and may work for certain supplement businesses.

However, approval timelines and pricing structures can vary depending on risk profile and processing history.

eMerchant Broker

eMerchant Broker offers support for both online and retail payment processing.

Like many general high-risk providers, the experience may depend heavily on the acquiring bank and business category.

Why Specialized High-Risk Processors Matter

Functional mushroom brands operate in a category that many traditional processors consider high-risk due to supplement regulations, wellness claims, and chargeback exposure.

Working with a processor that understands the industry can help reduce:

- Account shutdowns

- Fund holds

- Compliance issues

- Payment interruptions

- Chargeback risk

For brands focused on long-term growth, stability is often more important than simply getting approved quickly.

How to Get Approved for a Mushroom Merchant Account

To improve approval odds:

- Provide clear product descriptions (no exaggerated claims)

- Include lab testing or ingredient transparency

- Have a professional, compliant website

- Maintain a clear refund policy

- Show processing history (if available)

Working with a specialized provider dramatically increases approval success.

Final Thoughts: Choosing the Right Processor

For functional mushroom brands, payment processing isn’t just a backend tool, it’s a growth-critical decision.

The best processor will:

- Understand your industry

- Support compliance

- Provide long-term stability

For most brands, especially those in high-risk wellness categories, a specialized provider like Valmar offers the most reliable path forward.

Start here: https://stage.vlmr.com/mushroom-payment-processing/

Frequently Asked Questions

Can you legally accept payments for functional mushrooms?

Yes, if the products are legal and compliant, you can process payments through a high-risk merchant account.

Why do payment processors shut down mushroom businesses?

Some payment processors shut down mushroom businesses because they classify them as high-risk due to regulatory uncertainty and chargeback exposure.

What’s the safest way to process payments?

Use a dedicated high-risk merchant account provider, like Valmar – not Stripe or PayPal.

Can functional mushroom businesses use Stripe?

Some can initially, but many mushroom brands eventually face account reviews, frozen funds, or shutdowns due to high-risk classification.

Do mushroom businesses need a high-risk merchant account?

In most cases, yes. High-risk merchant accounts offer greater stability and are designed for supplement and wellness brands.

Are functional mushrooms considered high-risk?

Yes. Most payment processors classify functional mushroom brands as high-risk because of supplement regulations and chargeback concerns.

What payment processor is best for mushroom brands?

Specialized high-risk providers like Valmar are typically the best option for long-term stability and compliance support.

Why do Stripe and PayPal freeze mushroom business funds?

They use automated risk systems that often flag supplement and alternative wellness businesses as high-risk.

What causes payment processing applications to get denied?

Common reasons include unsupported health claims, incomplete compliance documentation, poor website policies, or lack of business history.

How can mushroom brands reduce chargebacks?

Using clear billing descriptors, transparent refund policies, fraud filters, and customer support can help lower disputes.

Is Valmar built for mushroom brands?

Yes. Valmar specializes in high-risk payment processing for functional wellness, CBD, supplement, and mushroom businesses.